By the time you finish reading this essay, at least one nation somewhere on Earth will have moved incrementally closer to crisis. Perhaps a central bank will have depleted its foreign reserves defending an unsustainable currency peg. Maybe a pension system will have slipped deeper into actuarial insolvency as another cohort reaches retirement age. Or possibly a political system will have inched closer to fragmentation as polarization intensifies.

We have sophisticated financial instruments to express views on nearly everything: corporate earnings, commodity prices, interest rate movements, all the way to the weather. Yet our ability to directly take positions on the trajectories of entire nations, particularly negative positions, remains surprisingly limited and fragmented.

As with all things, markets will push towards exploration, and our view is the development of comprehensive geopolitical financial instruments is not only inevitable but potentially beneficial for global stability, if properly designed and regulated.

I. The Missing Market

In October 2008, as Iceland’s banking system imploded, traders who had shorted the krona reaped enormous gains. They had identified classic vulnerability indicators: banking assets exceeding 1,000% of GDP, 80% of debt denominated in foreign currencies, a 15% current account deficit, and foreign exchange reserves covering just 30% of short-term debt. When crisis struck, the krona lost over half its value against the euro.

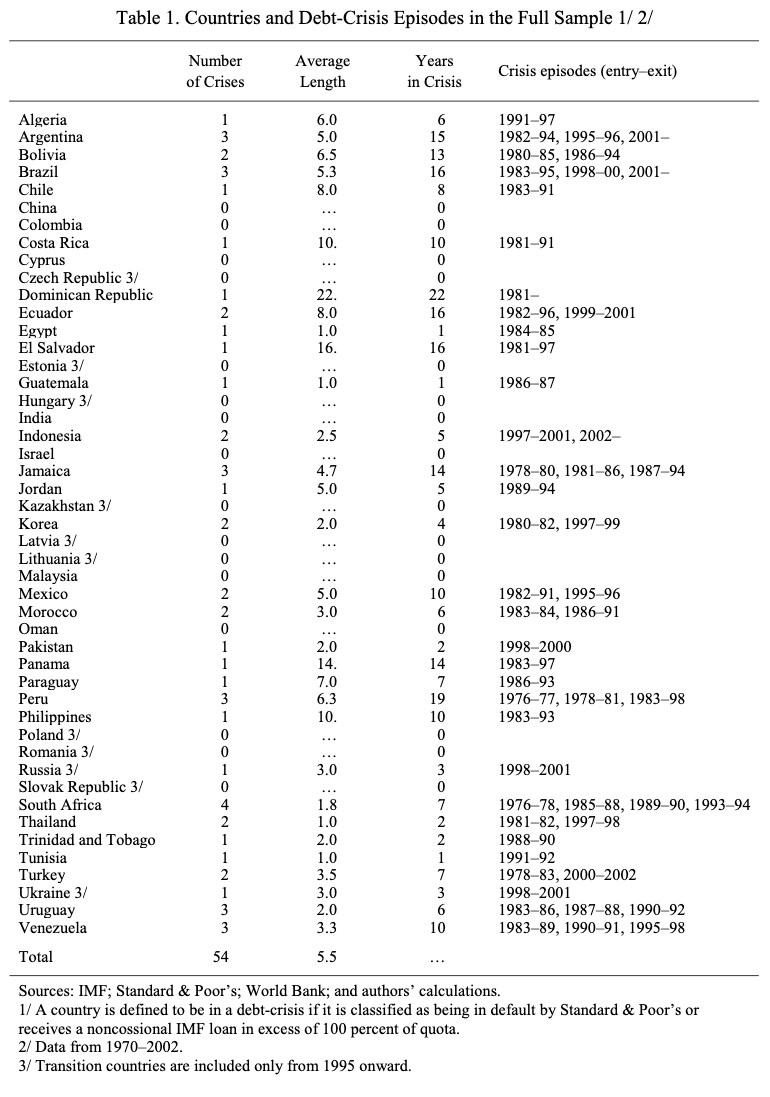

Historical data from the IMF reveals the frequency and patterns of sovereign debt crises across nations. Between 1970 and 2002, countries like Argentina, Brazil, and Peru experienced multiple debt crises, with some remaining in crisis for over a decade (see Figure 1).

This episode hints at what’s possible when financial markets enable direct bets against vulnerable sovereigns. But Iceland represented a limited case with traders primarily shorting its currency rather than taking comprehensive positions against the nation’s economic prospects. The tools for more holistic sovereign shorting remain underdeveloped.

Why does this market gap persist? The answer lies at the intersection of financial innovation, political sensitivity, and moral hazard.

Taking a negative position on a company is controversial enough; betting against an entire nation, with all the human consequences that entails, crosses boundaries that make many uncomfortable. Yet again, markets inevitably evolve toward completeness, filling gaps where risk transfer and price discovery create value.

One can look at the evolution of sovereign credit default swaps (CDS). When these instruments first gained prominence during the European debt crisis of 2010-2012, they were widely condemned as destabilizing speculation. German Chancellor Angela Merkel even attempted to ban “naked” sovereign CDS positions. Today, sovereign CDS are accepted components of the financial landscape, providing crucial signals about national creditworthiness.

The development of broader geopolitical financial instruments represents the next logical frontier in this evolution; moving beyond narrow credit perspectives to encompass the full spectrum of sovereign risk.

II. The Intelligence Problem

George Soros published an open letter in the Financial Times in 1998 arguing that the Thai baht’s fixed exchange rate was unsustainable. Within six months, Thailand’s currency collapsed, triggering the Asian Financial Crisis. To those paying attention, Soros was signaling the market positions of his Quantum Fund.

This anecdote illustrates a critical function of financial markets. They aggregate diverse, private information and analysis into actionable price signals. When it comes to sovereign trajectories, this information aggregation mechanism remains severely underdeveloped.

Another great example has been the challenge regarding China’s real estate sector in recent years. Despite widespread concerns about over-leverage and potential instability, the mechanisms for translating these concerns into clear market signals have been limited. Investors could short individual property developers like Evergrande or take positions on the yuan, but no instrument existed to directly express a negative thesis on the broader Chinese real estate ecosystem and its implications for national stability.

If we instead imagine a world with liquid markets for Chinese Institutional Stability Contracts or Demographic Transition Derivatives, precision may increase. Such instruments would provide continuous, real-time signals about market participants’ collective assessment of China’s vulnerability to property sector collapse and demographic aging.

These signals would benefit multiple stakeholders:

- Policymakers would gain early warning systems about emerging risks

- Businesses could more effectively hedge exposure to specific sovereign vulnerabilities

- Investors would have new mechanisms for portfolio diversification

- Citizens would receive clearer information about their nations’ challenges

Markets excel at processing complex, multidimensional information, precisely what’s needed to evaluate sovereign trajectories. We could imagine this being quite helpful today to the current Trump administration as well as US citizens who are being whiplashed weekly and are forced to process individual data points of chaos to understand second and third order economic effects.

III. The Instruments of Nation-State Speculation

While prediction markets today play a small role in time-bound, low liquidity, binary options surrounding economic indicators, we believe it’s worth exploring several categories of geopolitical instruments with a few concrete examples that could solve the liquidity and capital velocity issues present in prediction markets today.

Demographic Transition Derivatives

Japan stands as the world’s most advanced case of demographic aging, with its population declining by over half a million people annually. This demographic transition creates predictable strains on pension systems, healthcare infrastructure, and economic dynamism.

Table 2: Hypothetical projected Old-Age Dependency Ratios (Population 65+ per 100 Working Age Population)

| Country | 2025 | 2035 | 2045 | 2055 |

| Japan | 51.7 | 59.8 | 65.3 | 68.0 |

| Italy | 40.2 | 52.0 | 62.6 | 61.8 |

| Germany | 38.4 | 48.9 | 54.7 | 56.1 |

| South Korea | 30.1 | 49.6 | 65.6 | 70.1 |

| USA | 30.0 | 35.1 | 37.1 | 39.8 |

A Demographic Transition Derivative would enable investors to take positions on Japan’s ability to navigate these challenges. The instrument might reference metrics like old-age dependency ratio (projected to reach 68% by 2055), healthcare spending as percentage of GDP (10.74% in 2021), pension system funding gap (estimated at over 75 trillion yen), and labor force participation rates across age cohorts.

Settlement would occur based on predetermined thresholds for these metrics or pricing would be baked into a perpetual future of sorts. An investor bearish on Japan’s demographic resilience could purchase puts on these indicators, collecting payouts if they breach critical levels. Similar instruments could target other aging societies such as Italy, Germany, or South Korea where demographic transition creates systemic financial strain.

Political Fragmentation Indices

The January 6th, 2021 Capitol riot highlighted the potential for political polarization to threaten institutional stability even in established democracies. Similar pressures are visible globally, from Brazil’s political divisions to India’s religious tensions.

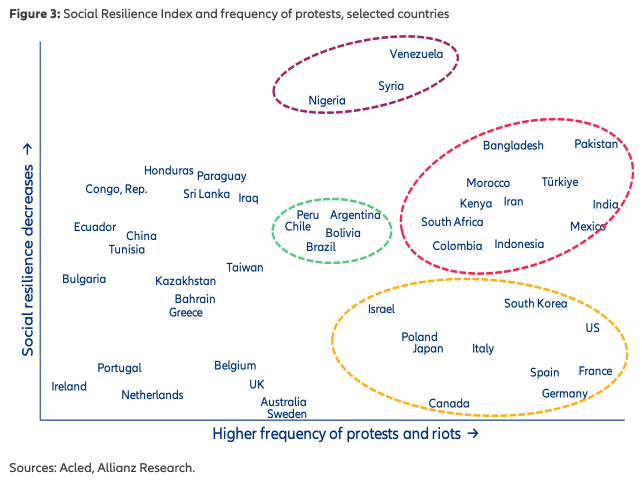

Recent data from Allianz Research captures this dynamic through their Social Resilience Index, which maps countries according to the frequency of protests and social resilience decreases (see Figure 2).

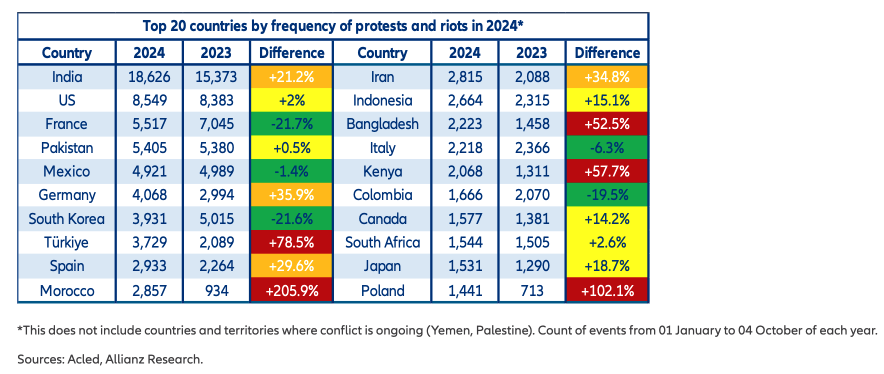

Nations like Venezuela, Syria, and Nigeria show concerning combinations of high protest frequency and declining social resilience. Further analysis of 2024 protest frequency data shows dramatic increases in countries like Morocco (+205%), Türkiye (+78.5%), and Poland (+102.1%), suggesting accelerating political fragmentation (see Figure 3).

Political Fragmentation Indices would enable positions on the stability of political systems based on quantifiable metrics: legislative gridlock measurements, political violence incidents, trust in government institutions, and electoral system functionality.

Interestingly, proxies for political instability already (very) loosely exist in cryptocurrencies. Bitcoin’s rise reflects, in part, a desire for assets governed by monetary principles without governmental risk. When citizens lose faith in their government’s monetary stewardship or institutional stability, cryptocurrency adoption often accelerates, as seen in Turkey, Argentina, and Venezuela. These organic market responses demonstrate demand for instruments that enable positioning against sovereign vulnerability.

While these instruments at first may not look to be able to properly price in “vibes” it’s likely that over time markets would trend to doing so.

Strategic Resource Vulnerability Swaps

When Russia restricted natural gas flows to Europe in 2022, Germany’s industrial base faced an existential threat. The nation had allowed itself to become critically dependent on Russian energy, creating a strategic vulnerability that manifested in economic terms.

Table 4: Critical Resource Dependency by Nation (Selected Examples)

| Resource | Critical Importer | Import dependency | Supply Concentration |

| Natural Gas | Germany | >70% of consumption | >40% from single source |

| Semiconductors | United States | >80% of advanced chips | >70% from Taiwan |

| Rare Earth | Japan | >90% of consumption | >60% from China |

| Phosphates | Brazil | >65% of consumption | >50% from Morocco |

| Water | Saudi Arabia | >70% of potable water | Desalination dependent |

Strategic Resource Vulnerability Swaps would allow positions on nations’ exposure to critical resource disruptions. This would be relevant for countries with concentrated strategic dependencies: Japan, which imports over 90% of its energy resources, with much from a limited number of Middle Eastern suppliers; Chile, whose economy depends heavily on copper exports; or Singapore, which imports over 90% of its food supply. In each case, the resource dependency creates specific economic vulnerabilities that could be priced and traded through specialized derivatives.

These instruments would reference metrics like import dependency percentages, supplier concentration indices, and stockpile adequacy. They would essentially price the premium a nation must pay for concentrated resource dependency, allowing investors to express views on resource security strategies while creating incentives for diversification.

Sovereign Resilience Options

Financial system stability represents another dimension of sovereign vulnerability. While investors can already express negative views on specific financial institutions through equity shorts or credit default swaps, Sovereign Resilience Options would enable broader positioning on a nation’s capacity to withstand systemic financial shocks (a la UBS or SVB). Unlike existing instruments focused on individual institutions, these would reference system-wide metrics like:

- Banking sector exposure relative to GDP

- Fiscal flexibility for bailouts

- Central bank independence metrics

- Cross-border financial contagion measures

This approach would complement single-institution perspectives by capturing the systemic dimensions of financial vulnerability that individual bank shorts miss. Furthermore, as institutions become increasingly interconnected, the value of synthetic instruments that aggregate and price system-wide risks grows accordingly.

IV. The Strategic Dynamics of Sovereign Shorting

In May 2010, as Greek bond yields soared during the European debt crisis, a battle unfolded between hedge funds shorting Greek debt and European institutions attempting to stabilize the situation. The ECB ultimately launched unprecedented intervention programs, but not before the market took its pound of flesh for Greece’s fiscal excesses.

This episode illustrates the complex strategic game that unfolds when participants can take substantial positions against sovereign entities. Unlike traditional securities, where market positions have minimal impact on underlying fundamentals, sovereign shorting can create feedback loops that potentially validate the initial thesis.

These dynamics create both risks and benefits:

The Self-Fulfilling Prophecy Problem

Large short positions against sovereign entities can potentially trigger the very outcomes speculators anticipate. If investors massively short Italy’s Demographic Transition Derivatives, this could:

- Increase Italy’s borrowing costs as lenders incorporate this negative signal

- Accelerate capital flight as domestic investors hedge exposure

- Complicate political efforts to implement necessary reforms

- Reduce foreign direct investment due to heightened perceived risk

This dynamic creates genuine moral hazard with the potential for speculation to harm real economic outcomes. However, this concern must be balanced against a crucial counterpoint that we believe may make all these risks worth it.

The Early Warning Benefit

The world is filled with more noise than ever before leading to strange optimizations and at times, seemingly nonsensical decisions made by governments, institutions, and individuals.

Market signals provide invaluable early warnings about unsustainable policies or vulnerabilities. Greece’s debt dynamics were objectively problematic long before the crisis erupted—shorting pressure simply forced recognition of this reality.

Lebanon provides a stark recent example. For years, the nation maintained an unsustainable currency peg and banking system while ignoring mounting warning signs. When the system finally collapsed in 2019, the adjustment was catastrophic—the Lebanese pound lost over 90% of its value, wiping out savings and triggering hyperinflation.

More developed geopolitical financial markets might have forced earlier, more orderly adjustment through clearer shorting signals before total collapse became inevitable. Empirical evidence supports this view: comparing sovereign crises across the past three decades, nations that received early market signals approximately 6-24 months before full crisis generally experienced GDP contractions 50-70% less severe than those that faced sudden adjustment.

This isn’t dissimilar to some of the arguments for Decentralized Finance and the FTX Scandal. During the implosion of FTX, many centralized players with dark pools of debt and unsecured non-transparent leverage caused massive holes in balance sheets and people’s wallets, which is in contrast to the orderly liquidations that happened for transparent (and admittedly overcollateralized) pools of capital on-chain.

Manipulative Scenarios

The most troubling scenario involves strategic manipulation; actors taking large short positions and then actively working to ensure their success. One could imagine a theoretical fund that:

- Establishes massive short positions against a vulnerable democracy

- Funds disinformation campaigns to exacerbate political division

- Uses media connections to amplify negative narratives

- Provokes policy responses that damage economic stability

This isn’t entirely theoretical. Questions persist about whether hedge funds actively undermined Greek stability during the eurozone crisis through information operations alongside their market positions.

However, such manipulation becomes significantly harder in liquid, transparent markets with appropriate position limits and disclosure requirements. The solution is proper market design, not prohibition.

V. The Ethics of Betting Against Nations

When the British pound plummeted following the announcement of Liz Truss’s ill-conceived mini-budget in 2022, hedge funds that had shorted the currency realized substantial profits, while British citizens faced economic uncertainty.

This raises profound ethical questions: Is it morally acceptable to profit from sovereign distress? Does betting against nations cross a line that corporate shorting does not?

These concerns are valid but must be weighed against the alternatives. A world without sovereign shorting does not necessarily eliminate sovereign vulnerability or the next-order effects of collapse, it merely obscures it until crisis erupts.

One can think of a few different frameworks from consequentialist (If geopolitical financial markets accelerate necessary policy adjustments while preventing more severe crises, they may produce net positive outcomes despite creating winners and losers) all the way to distributive justice (Market participants reap profits while vulnerable populations often bear adjustment costs; this legitimate concern suggests the need for complementary social protection mechanisms rather than prohibiting the markets themselves).

The ethics remain complex, but a balanced view recognizes that information markets don’t create underlying vulnerabilities but instead reveal them, potentially enabling earlier and more orderly responses.

VI. Implementation and Governance

How might a more comprehensive system of geopolitical financial instruments emerge responsibly? While there is significantly more research to be done here there is some precedent.

Graduated Implementation

Beginning with more stable nations and well-defined metrics would allow market mechanisms and regulatory frameworks to co-evolve. An initial focus on OECD countries with robust institutions would minimize disruption while establishing precedents.

The European Financial Stability Facility (later ESM) created during the eurozone crisis offers a partial template. It initially focused on more developed economies before extending to periphery nations, allowing mechanisms to mature gradually.

Transparent Information Framework

Standardized, objective sovereign metrics with robust calculation methodologies would anchor contract settlement. Independent third-party calculation agents, similar to those verifying ISDA credit events, would determine outcomes based on predetermined criteria.

Crisis Circuit Breakers

Automatic position reduction mechanisms during extreme sovereign stress would prevent destabilizing feedback loops. Similar to equity market circuit breakers, these would activate when shorting pressure exceeds predetermined thresholds, forcing gradual position reduction rather than panic liquidation.

VII. Market Evolution Projections

With this in mind, we imagine the evolutionary path for geopolitical financial instruments would likely unfold in retrospectively distinct phases:

Phase One: From Prediction Markets to Shadow Markets (2025-2030)

The foundations for geopolitical financial instruments are already visible in today’s prediction markets like Polymarket and Kalshi, which offer time-based binary options on events ranging from election outcomes to international conflicts and economic indicators. These platforms represent primitive but functioning prototypes for sovereign risk markets, though with significant limitations in scope, liquidity, and regulatory status.

By 2025-2030, we’ll likely see two parallel evolutionary paths:

- Expanded Prediction Markets: Platforms like Polymarket, Kalshi, and new entrants will gradually extend beyond simple binary outcomes to more nuanced, multi-dimensional predictions about sovereign stability. Rather than asking “Will Country X default by date Y?”, these platforms will develop more sophisticated conditional markets addressing specific vulnerability dimensions.

- Institutional Shadow Markets: Simultaneously, more sophisticated bilateral, over-the-counter contracts will emerge between institutional investors. Initially resembling private wagers more than formal financial products, these instruments would trade in limited circles with minimal regulatory oversight, somewhat like early credit default swaps in the 1990s.

Major investment banks could towards 2030 begin forming specialized geopolitical risk desks. Early adopters would include hedge funds with substantial macroeconomic focuses, sovereign wealth funds seeking to hedge against regional competitors, and family offices of ultra-high-net-worth individuals from politically unstable regions.

Preferred early targets would include smaller nations with clearly quantifiable vulnerabilities: countries with unsustainable debt trajectories, extreme demographic challenges, or concentrated resource dependencies. Trading volumes would remain modest, but significant alpha would accrue to early participants willing to build specialization while also deal with the liquidity and mark-to-market complexities that novel instruments present.

Phase Two: Standardization and Exchange Trading (2030-2035)

As private markets demonstrate the viability of these instruments, exchanges would begin offering standardized contracts on a limited set of sovereign metrics.

Regulatory frameworks would evolve to address the unique challenges of geopolitical instruments, with particular focus on insider trading (how to define material non-public information about sovereign events), manipulation (position limits and disclosure requirements), and settlement disputes (independent verification mechanisms).

Financial innovation would accelerate as data providers develop increasingly sophisticated sovereign risk metrics. Bloomberg or a set of specialized startups would compete to create the definitive indices for monitoring institutional stability, resource security, and demographic transition risks. Investment strategies would emerge around seasonal patterns in political risk, correlation trading between different sovereign vulnerabilities, and pairs trading between competing nations.

Likely more experimental instruments would be brought on-chain to drive down spread due to efficiencies presented by public blockchains and smart contracts.

Phase Three: Mass Market Integration (2035-2040)

By this stage, geopolitical financial instruments would become integrated into mainstream portfolio management. Retail-focused ETFs would offer exposure to baskets of countries sorted by stability characteristics. Pension funds would routinely hedge their domestic political risk exposure through offsetting international positions. Central banks might even utilize these markets for policy signaling.

The existence of liquid, transparent markets for sovereign risk would fundamentally alter international relations. Nations would face immediate financial consequences for institutional deterioration, creating powerful incentives for governance improvements. Political leaders would closely monitor market-implied probabilities of instability much as they currently track bond yields and currency values.

Some authoritarian regimes would attempt to manipulate these markets, buying up contracts that signal instability to prevent negative signals. However, the market’s size and liquidity would eventually make such manipulation prohibitively expensive, much as central banks have found currency market intervention increasingly difficult as global forex trading volumes expanded.

Phase Four: Institutional Adaptation (2040-2050)

As geopolitical financial markets mature, institutional structures would evolve in response. New international bodies might emerge to establish standard metrics for sovereign stability assessment. Academic disciplines would develop around the study of sovereign vulnerability pricing efficiency.

Nations would increasingly incorporate market signals into policy planning. Finance ministries might establish specialized “market signal interpretation” units to decode what geopolitical instrument pricing reveals about perceived vulnerabilities. Some forward-thinking governments might even use adverse market signals as political cover for difficult but necessary reforms.

Meanwhile, the most sophisticated investment strategies would move beyond simple directional bets on sovereign instability toward complex, multi-factor approaches. Funds might simultaneously hold long positions in a nation’s technological innovation capacity while shorting its institutional stability, expressing nuanced views on the interaction between different aspects of sovereign performance.

Of course, with all of these progressions, AI will play an important role.

VIII. Unintended Consequences and Adaptive Responses

The establishment of geopolitical financial markets would inevitably produce unintended consequences, both positive and negative:

Sovereignty Arbitrage

As markets efficiently price sovereign risks, capital would flow toward governance models offering superior risk-adjusted returns. Nations might compete to improve their stability metrics, creating a form of “sovereignty arbitrage” where reforms are implemented specifically to improve market perceptions. While potentially beneficial, this could also lead to superficial changes designed to game the metrics rather than implement substantive reforms.

Information Warfare Evolution

The existence of markets that directly price sovereign stability would transform information warfare. At a time where we already are worried about the 4o studio-ghiblification of all content, information warfare could become more destructive and impactful than we have ever imagined. Hostile actors might seed disinformation specifically designed to influence geopolitical instrument pricing, creating a new attack vector against national financial stability. This would necessitate specialized defenses against “market perception manipulation” as a component of national security strategy, as well as stricter laws surrounding doing so.

Reflexivity Challenges

The mutual influence between market pricing and underlying fundamentals would create complex reflexive dynamics. George Soros’s theory of reflexivity, where market perceptions and reality influence each other in a feedback loop, would manifest powerfully in geopolitical financial markets. Some nations might experience “stability runs” similar to bank runs, where declining market confidence triggers real deterioration, further reducing confidence.

Power Redistribution

Perhaps most profoundly, geopolitical financial instruments would redistribute power between sovereign entities and market participants. The immediate feedback provided by these markets would constrain sovereign decision-making in new ways, particularly for nations dependent on external financing. While potentially beneficial for global stability, this raises legitimate questions about democratic accountability when market mechanisms constrain elected governments.

Conclusion: Creative Destruction for Nations

Joseph Schumpeter’s concept of “creative destruction” describes how market forces continuously replace outdated economic structures with more efficient ones. This process traditionally applies to companies and industries.

Despite the rise and fall of various empires, over the past few centuries, nations have largely been shielded from this discipline. While sovereign defaults occur, the underlying political and institutional structures often persist even when fundamentally unviable. The result is zombification; nations that neither truly fail nor meaningfully reform, trapping citizens in prolonged decline.

A more complete ecosystem of geopolitical financial instruments would introduce a measured form of Schumpeterian discipline to sovereign entities. This could perhaps lead to less chaotic destruction of sudden crises, but instead a continuous feedback of market signals highlighting specific vulnerabilities and rewarding their resolution.

In a world of increasing complexity and interconnection, we need more sophisticated mechanisms for identifying and addressing sovereign fragility. Properly designed markets for geopolitical risk transfer, including sovereign shorting, could represent one of our most promising tools for navigating these challenges.

The stability of our future may depend less on shielding nations from market discipline than on ensuring that discipline operates continuously rather than catastrophically, preventing bigger crises through the early recognition of smaller ones.

Leave a Reply